In a market where visibility has reached its peak, the conditions that determine which brands endure have changed. Growth is no longer sufficient to sustain every brand. As pressure increases, the difference between perception and structural reality becomes more visible.

This paper introduces a framework to evaluate agave spirits brands beyond surface-level signals: Built Right. Brought Right. This is not a message; it is a system for understanding how brands are constructed, how they perform in the market, and whether they can sustain both under pressure. The framework combines structural evaluation, market behavior, and observable signals to identify which brands are built to hold—and which are not.

This framework is not intended as a statement of beliefs. It is intended as a tool for evaluating brands under real market conditions.

The principles outlined here only matter if they can be observed, tested, and applied in practice.

The following sections translate these principles into observable variables and decision behavior, particularly under conditions where pressure and trade-offs are present.

Because in a tightening market, outcomes are not determined by intention. They are determined by how decisions are made when conditions become difficult.

Over the past decade working inside the agave category, we have seen visibility reach levels that would have been difficult to imagine.

Growth has been extraordinary. New brands entered rapidly, consumer interest expanded, and global awareness reached new heights. At the same time, the category has become harder to navigate:

More recently, growth has slowed and, in some cases, begun to contract. As momentum stabilizes, pressure is no longer theoretical—it is being felt. The market is no longer expanding fast enough to carry every brand forward. Brands that entered during expansion are now being tested under constraint.

We have seen brands succeed and fail under the same conditions. This confirms that visibility does not determine success; structure and execution do.

Retail performance is also becoming more selective. We are seeing overall softness in the category alongside continued growth in structurally differentiated segments. Retail decision-making is increasingly driven by velocity, margin contribution, and repeat demand rather than expansion alone. This has made placement more selective and harder to sustain over time.

These observations are drawn from direct participation in brand building, distribution, and retail execution across multiple markets. This is not a personal statement—it is a framework built from observed patterns and applied experience in the market.

For several years, much of the discussion around agave spirits has centered on ingredients.

These conversations helped elevate awareness and move the category forward.

But they are no longer enough.

Ingredient transparency does not answer the questions that matter under pressure:

In our experience, the market is moving beyond a single-variable conversation.

A more complete framework is required.

Recent consumer research, including work by Jay Baer, shows increasing awareness around production, transparency, and authenticity.

These signals represent progress.

But they remain incomplete.

Consumers are learning how to choose.

The market is learning how to filter.

Retail behavior reflects a transitional market in which consumer demand remains attached to terms such as additive free even as the language used to classify those products begins to change.

Recent retail data suggests that growth is increasingly concentrated at the extremes of the market, with value-driven and structurally differentiated brands outperforming the middle.

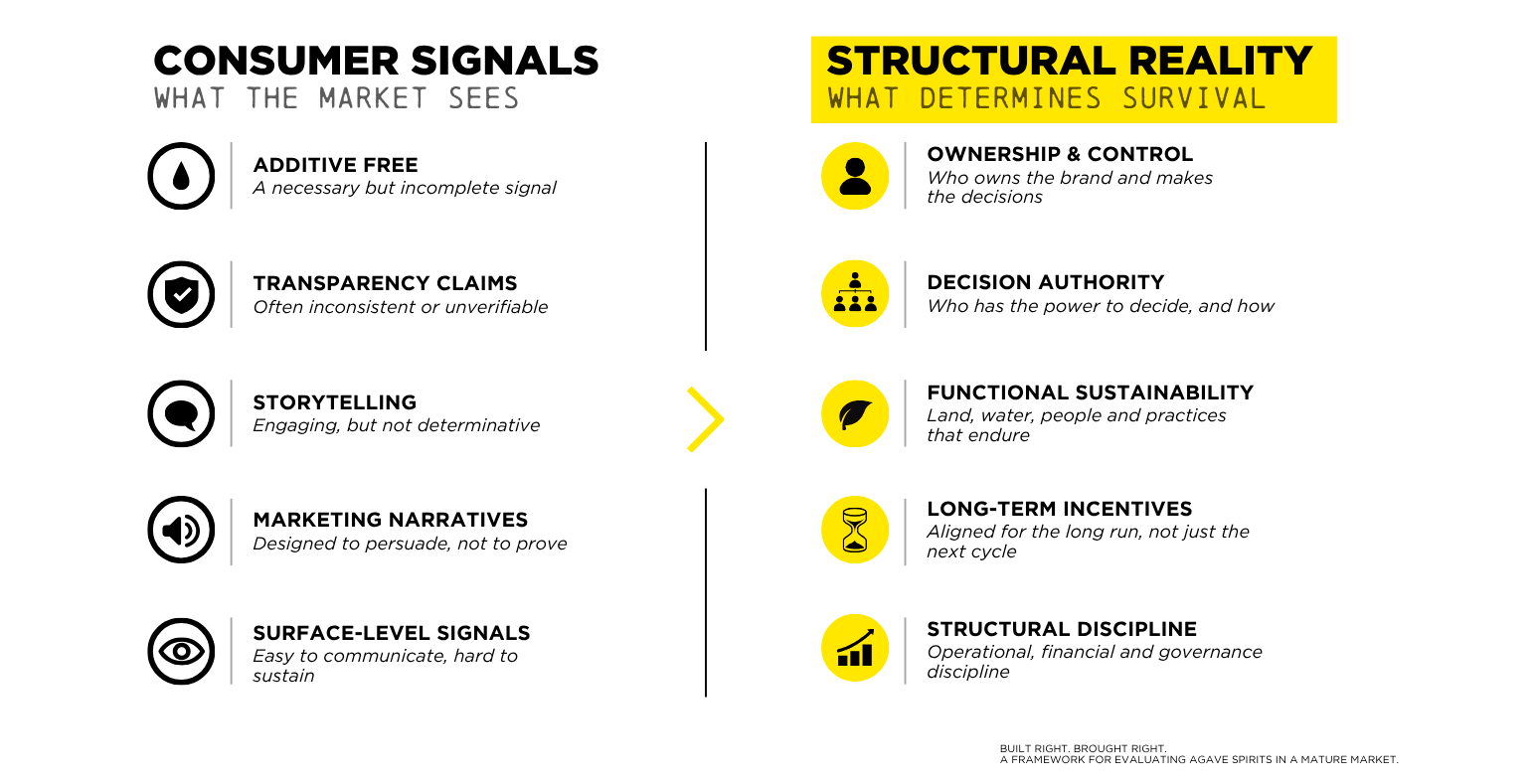

Most current signals used to evaluate brands are surface-level. They do not reliably indicate how a brand will behave under pressure.

We have found that a system is required—one that evaluates not just what a product is, but how it is built and how it is brought to market. This framework is derived from what has held up under pressure, rather than from theory alone.

As pressure increases, the question is no longer whether a brand can enter the market; the question is whether it can justify its place within it over time.

We have seen brands enter the market with real momentum, only to struggle when that momentum slows. Within this framework:

.png)

.png)

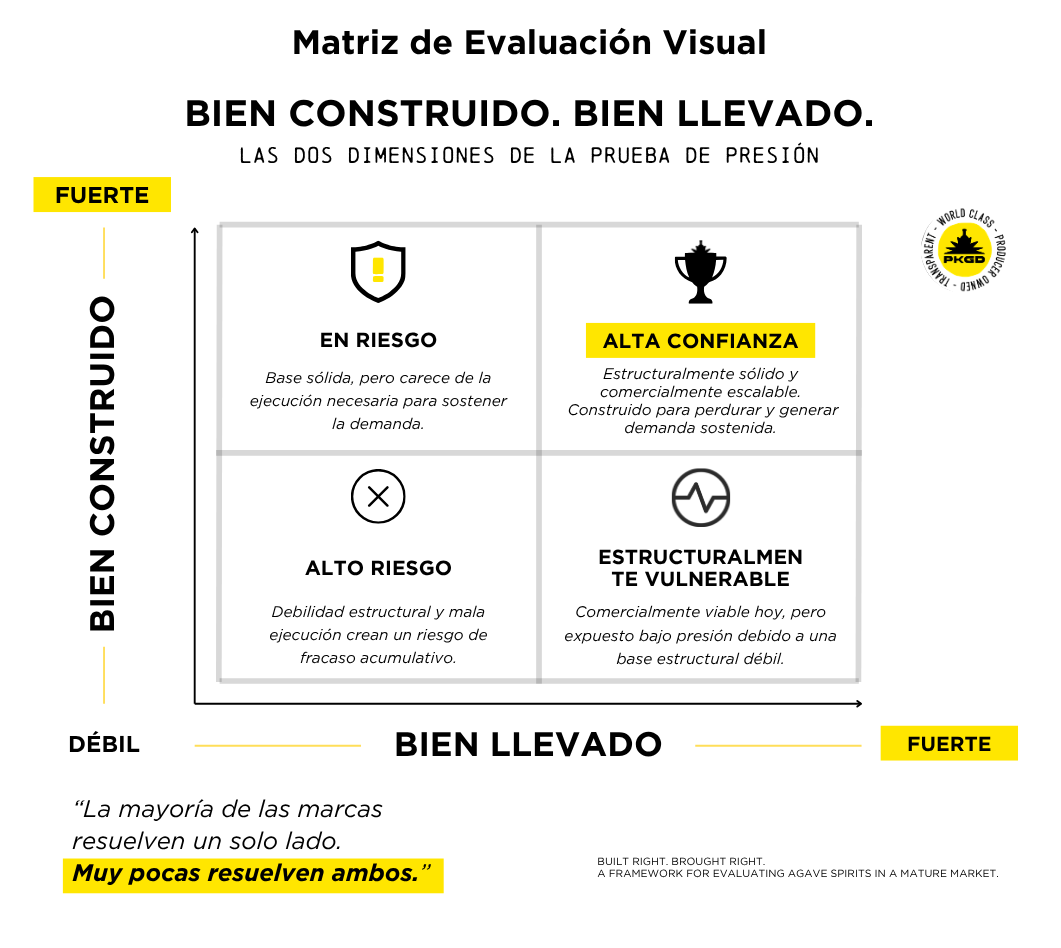

The true character of a brand is revealed under pressure. However, not all pressure is applied at the point of production.

Some brands fail not because they are made incorrectly, but because they are not brought to market in a way that creates or sustains demand. Distribution gaps, weak positioning, and lack of consumer pull can quietly erode a brand, regardless of how well it is made. This is the second dimension of the Pressure Test.

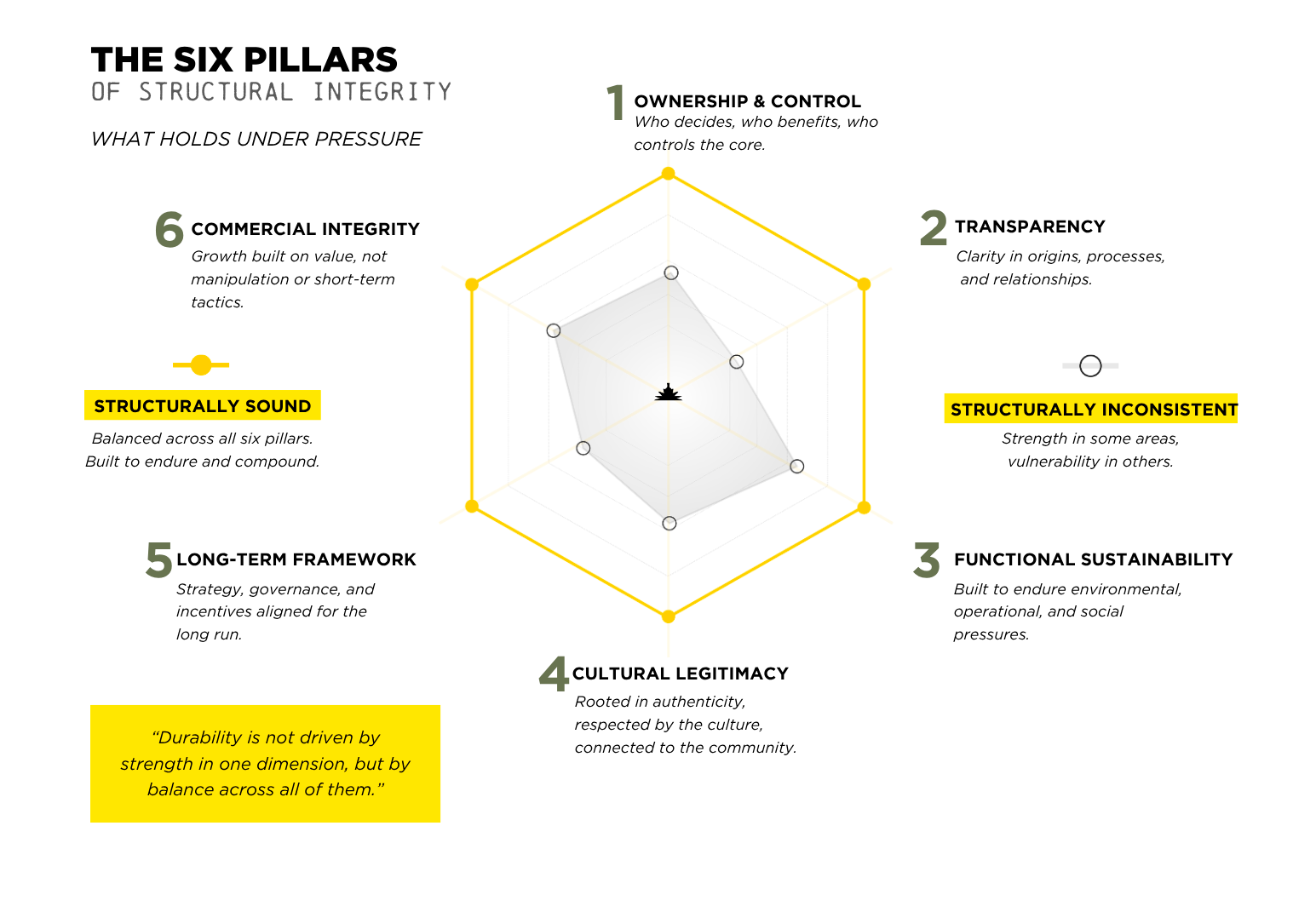

The Six Pillars define the conditions that must hold for a brand to sustain integrity under pressure.

We have observed consistent patterns over time. Brands that align with these principles tend to maintain product integrity and generate sustainable demand. Brands that do not often rely on short-term momentum that becomes difficult to sustain under pressure. While comprehensive market-wide data is limited, these patterns have repeated across multiple market cycles and contexts.

.png)

Who owns the brand is the starting point; who controls the decisions is the test.

“Maintaining control over production decisions is what allows the product to remain consistent, regardless of external pressure.”

— Felipe Camarena, G4 Tequila / El Pandillo

Jesús María, Jalisco, MX.

A brand qualifies as Built Right only if:

Without this structural foundation, control becomes conditional when market or financial pressures mount.

Producer Controlled is not a philosophical position. It is a structural requirement.

To meet this standard, production decision authority must be clearly defined and protected within governing agreements.

This authority must not be subject to override by investors, brand ownership structures, or intellectual property control.

If this authority is not explicitly written and enforceable, it will not hold under pressure.

External capital does not disqualify a brand from meeting this standard.

Loss of decision authority does.

Transparency is not a claim; it is a behavior.

“Transparency is a responsibility, especially when representing traditional processes to a wider market.”

— Roberto Real, Tequila Ancestral Arriesgado / Tequila Selecto

Amatitán, Jalisco, MX.

True transparency includes:

Sustainability must function under pressure.

“Water is essential… we treat vinazas and reuse water in the process.”

— Carlos Méndez Blas, Mezcal Palomo

Santiago Matatlán, Oaxaca, MX.

“We’ve worked hard to reduce water consumption… 100% of bagasse and vinazas are converted into compost.”

— Eduardo Orendain Jr., Tequila Arette

Tequila, Jalisco, MX.

Sustainability must be demonstrable in practice, not narrative. When sustainability does not function under pressure, the consequence is not theoretical. It becomes operational.

Agave spirits are cultural products.

“The work is not just about making tequila, but continuing a process that belongs to the family and the place.”

— Chava Rosales, Cascahuín

El Arenal, Jalisco, MX.

Legitimacy reflects:

When this connection is broken, legitimacy does not disappear immediately. It erodes over time.

Short-term growth is not the objective.

Durability is:

“Decisions are made with future generations in mind.”

—Juan Eduardo Núñez, Tequila El Viejito

Atotonilco, Jalisco, MX.

“We prefer to grow in a sustainable way, not with shortcuts.”

— Eduardo Orendain Jr., Tequila Arette

Tequila, Jalisco, MX.

“Growth has to respect the rhythm of the land.”

— Fausto Romero, Raicilla El Acabo.

El Asil Ahuacatepec, Jalisco, MX.

Momentum can accelerate growth. It can also conceal structural weakness.

Commercial integrity is not only about protecting a brand.

It is about building real, sustained demand.

“Responsibility extends beyond making the product… to how it is represented in the market.”

— Luis Ángel Villalobos, Tequila El Ateo

Romita, Guanajuato, MX.

“We all want growth… but it must be done with ethics and contribute to the community.”

— Sergio Vivanco, Destilería Viva México

Arandas, Jalisco, MX.

Brought Right requires:

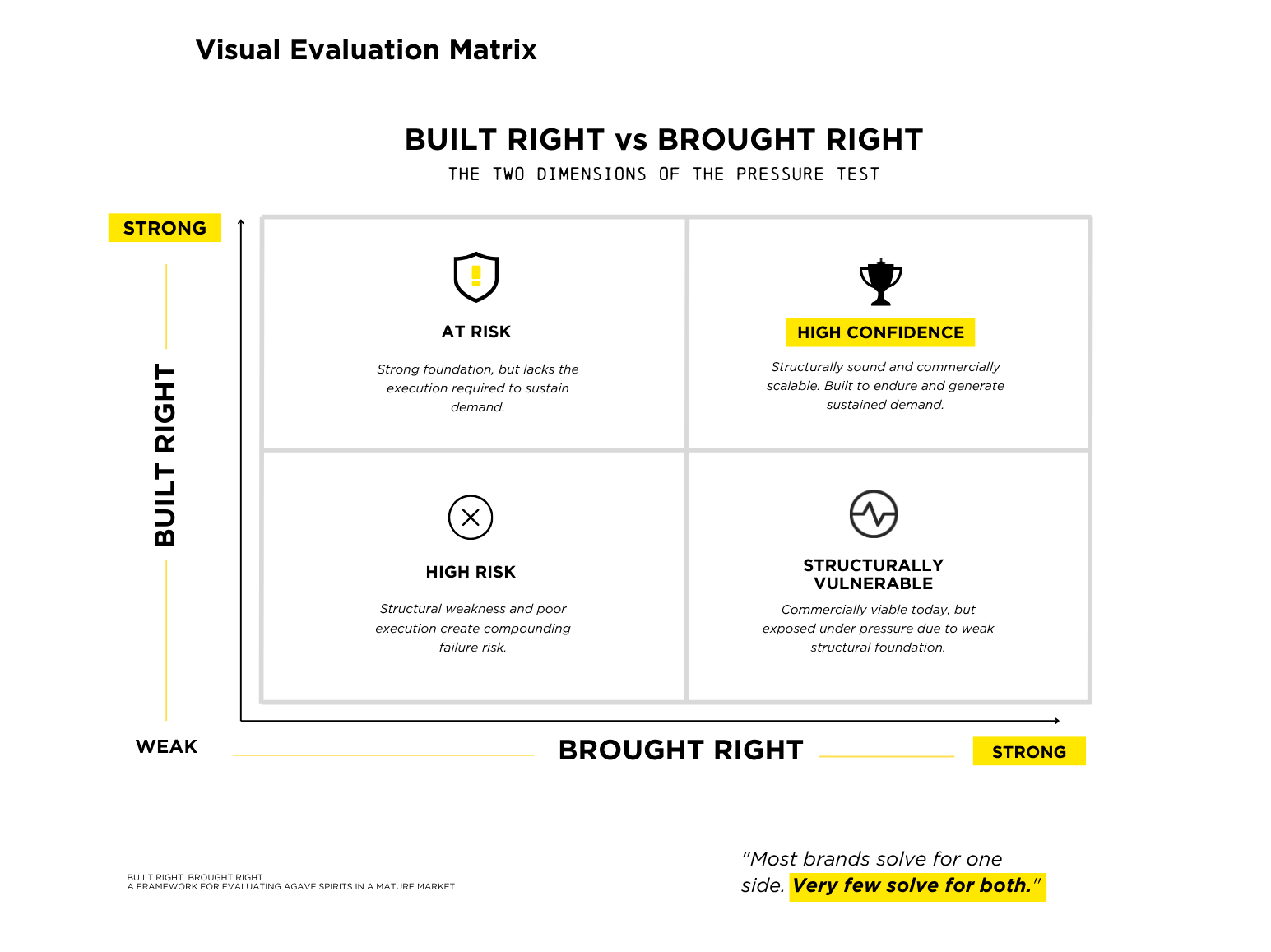

Most brands solve for only one side of the equation; very few solve for both. Crucially, solving for one does not compensate for the absence of the other.

Determines whether a product can endure.

Built Right is not an abstract concept. It is defined by structural variables that can be evaluated.

These include:

The presence of these variables is not sufficient on its own. The critical question is whether they hold under pressure.

Determines whether a product survives commercially.

Brought Right is expressed through observable market behavior.

Key variables include:

These variables determine whether a brand is being brought to market in a way that supports long-term sustainability.

In a tightening market, principles do not exist in isolation. They are tested through trade-offs.

Common pressure points include:

These moments are not exceptions. They are the conditions that define outcomes.

The distinction between brands that endure and those that do not is not whether they face pressure, but how decisions are made under it.

Brands that maintain decision integrity under pressure protect the long-term value of the product.

Brands that do not may achieve short-term gains, but introduce structural erosion over time.

The restructuring of the U.S. distribution landscape reinforces a central argument of this paper: access to the market is not the same as execution in the market.

As national distribution models come under pressure, suppliers are no longer prioritizing theoretical 50 state coverage. They are prioritizing operational reliability, regional strength, and the ability to deliver results at the account level.

Recent realignments across major distributors reflect this shift. Large scale national platforms are fragmenting into regional operators with stronger local execution, while others are expanding capabilities across beer, spirits, and emerging beverage categories to remain relevant.

This is not simply a distributor story. It is a structural signal.

The middle tier is undergoing the same pressure test as brands.

Under pressure, the question is no longer who can carry the most brands. The question is who can create focus, drive velocity, and convert placement into repeat demand.

For producer owned brands, this distinction is critical. Being listed is not enough. Being actively supported in the right markets, with aligned incentives and clear execution, is what determines whether production integrity translates into sustainable growth.

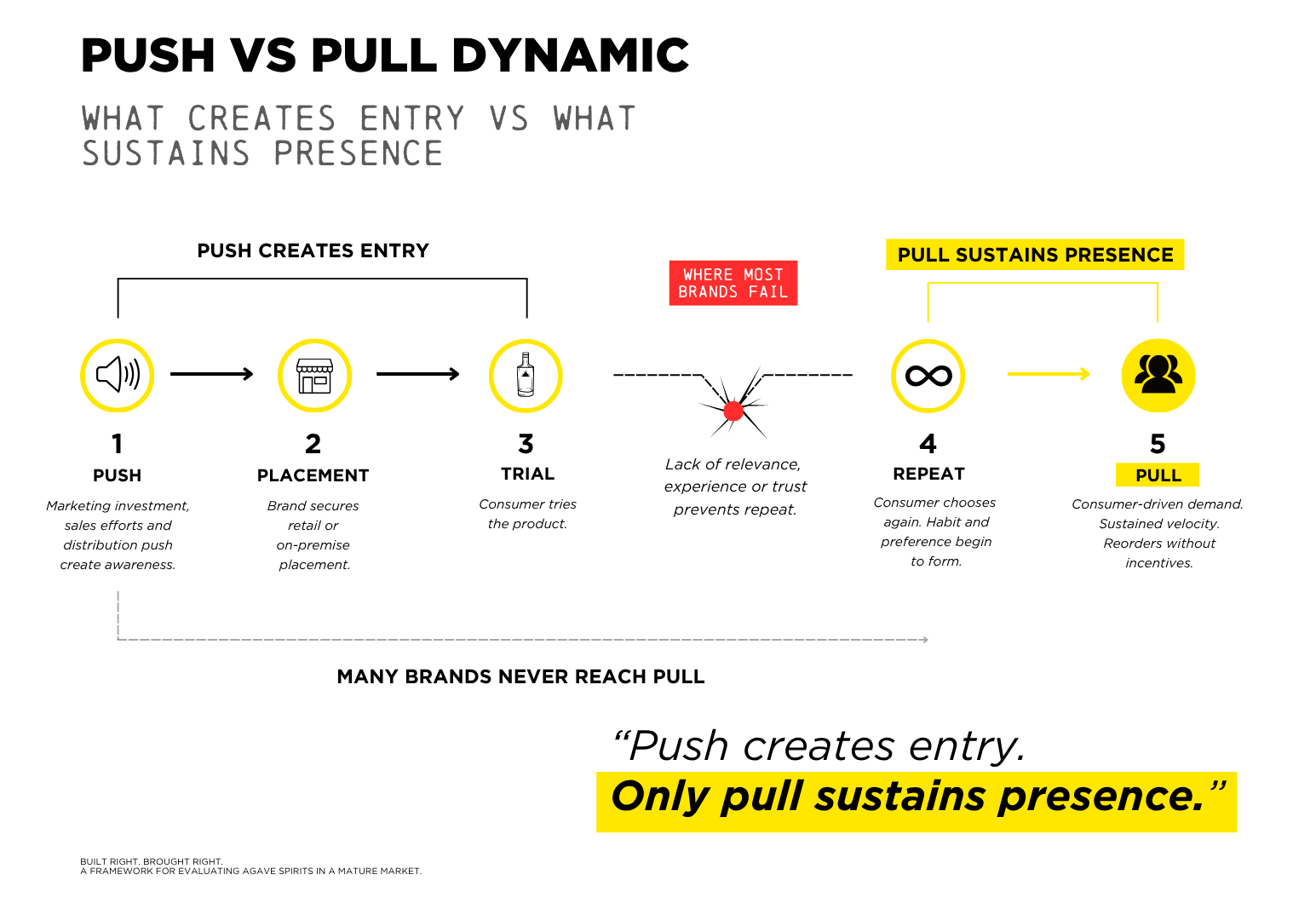

Push is required to enter the market, but if that push does not convert into pull, the brand becomes perpetually dependent on it.

Brought Right also requires that a product be discoverable, intelligible, and correctly framed at the point of search and sale. This includes how it is categorized, how it is described, and how easily a consumer can understand what differentiates it in a crowded set.

Observable signals of "pull" include:

The Operational Reality:

All brands require support.

The distinction is whether that support reinforces demand or substitutes for it.

Sustained push without conversion to pull increases long-term risk for both supplier and retailer.

In practice, this risk often presents in consistent patterns:

Implication:

If a brand does not demonstrate conversion from push to pull over time, it should be reevaluated regardless of initial placement success.

Important Clarification

This framework does not judge products by taste.

It evaluates whether the structure protects the product from being changed by commercial pressure.

Some brands are built correctly at every level of production, yet fail due to weak execution. This is not a product failure; it is a market failure, and the outcome is the same.

We have participated in these decisions in real time and observed a fundamental division of labor:

When both are aligned, the system holds.

This framework is not a compliance system. However, real demand and effective execution can be observed through signals such as:

These signals help distinguish structural demand from temporary performance. They do not define success; they indicate whether that success is real.

Additional indicators may include successful search conversion, expansion following strong performance in initial test markets, and repeat purchases following assisted engagement or guided tastings.

.png)

What matters is not what a brand says.

What matters is how it is built and how it performs under pressure.

Built Right. Brought Right. is not a message. It is a system for evaluation.

This framework is not a certification system. It is a tool for evaluating structure and performance under pressure. Specifically:

Across regions and traditions, the message remains consistent. The following producers and partners represent the structural integrity and market behavior defined by this framework.

Tequila (Jalisco & Guanajuato)

Mezcal

Raicilla

Different regions. Different traditions.

Aligned principles: Responsibility, discipline, and continuity.

As pressure increases, differentiation becomes clearer. The market will not reward every brand. It will reward the ones that hold.

But this moment is not just a filter.

It is a shift.

For years, growth allowed many brands to participate without being fully tested. Visibility created the appearance of strength. Placement created the appearance of demand. Momentum masked structural weaknesses.

That phase is ending.

As the market tightens:

What begins to matter now is whether a brand can convert its structure into sustained demand. Not once, but repeatedly. Under pressure.

This is where the distinction between Built Right and Brought Right becomes decisive.

Both fail. Just at different speeds.

Pressure is not only a function of decline.

It is often created by success.

Growth introduces its own constraints:

What holds under these conditions defines long-term outcomes.

The opportunity is not simply to survive this shift.

It is to emerge from it with clarity.

To understand not just what a brand is, but how it behaves when tested.

To build systems that do not depend on ideal conditions.

To align production, positioning, and market execution in a way that can hold over time.

In a less forgiving market, clarity becomes an advantage. And for those who are built and brought correctly, pressure is not a threat.

It is validation.

For distributors, this framework provides a way to evaluate which brands will convert demand into sustained velocity, not just initial placement.

For retailers, it provides a way to distinguish between brands that generate repeat purchase and those that rely on continued support to maintain movement.

For brand owners, it defines the conditions required to build a business that can endure beyond early growth and operate consistently under pressure.

In practice, the application is not theoretical. It shows up in decisions:

The objective is not to optimize for entry.

It is to build for endurance.

In each case, the question is the same:

Is this brand structurally positioned to sustain performance as conditions tighten, or is it dependent on conditions that may not hold?

Being built correctly is not enough.

A brand must also be brought to market in a way that creates and sustains real demand.

Ultimately, the market determines which brands hold and which do not.

This framework is an attempt to understand why.

It is not a theory built in isolation. It reflects patterns observed across producers, brands, distributors, and retailers operating under real conditions.

Across those observations, one truth becomes consistent:

Without demand, discipline becomes irrelevant.

Without discipline, demand becomes destructive.

The brands that endure are not defined by a single advantage.

They are defined by alignment.

This is what allows a brand to navigate pressure without compromising what made it valuable in the first place.

This framework does not determine what tastes best.

It determines what holds.

The next phase of the category will not be defined by who participates.

It will be defined by who is structured to withstand pressure and who is not.

Growth will continue, but not evenly.

Attention will remain, but not indefinitely.

And the gap between perception and reality will continue to close.

The market is no longer asking who can enter.

It is revealing who can remain.

Built Right. Brought Right. Is not a message, it is a standard.

All producer insights included in this document were collected directly through interviews, written responses, and documented conversations between January and March 2026.

Quotes have been translated and edited for clarity where necessary.

Their inclusion provides perspective from within the category and does not imply endorsement of this framework or its conclusions.

PKGD Built Right. Brought Right.

The framework can be applied in practice through a simplified evaluation tool: Purpose

A rapid evaluation tool to assess whether a brand is structurally sound and commercially viable under pressure.

1. Control

Does the producer retain final, non-overridable authority over decisions that affect the product?

☐ Yes ☐ No

2. Consistency Under Pressure

If costs rise or supply tightens, is the product likely to remain unchanged?

☐ Yes ☐ No

3. Transparency as Behavior

Is transparency demonstrated through actions, not just claims?

☐ Yes ☐ No

4. Sustainability That Functions

Are environmental and production practices operational and maintained under pressure?

☐ Yes ☐ No

5. Cultural Legitimacy

Is the product meaningfully connected to its place, process, and people?

☐ Yes ☐ No

Built Right Result

☐ Strong (4–5 Yes)

☐ Conditional (2–3 Yes)

☐ Weak (0–1 Yes)

6. Demand Creation

Is there clear evidence of consumer pull beyond initial placement?

☐ Yes ☐ No

7. Conversion (Push to Pull)

Does initial support convert into repeat purchases and reorders?

☐ Yes ☐ No

8. Velocity Consistency

Does the product move consistently across comparable accounts?

☐ Yes ☐ No

9. Pricing Integrity

Does the brand maintain pricing without relying on continuous incentives?

☐ Yes ☐ No

10. Shelf and Search Clarity

Is the product easy to understand, categorize, and differentiate at point of sale?

☐ Yes ☐ No

Brought Right Result

☐ Strong (4–5 Yes)

☐ Conditional (2–3 Yes)

☐ Weak (0–1 Yes)

.png)

It reflects a simple reality: product alone does not determine success, and momentum without structure does not last.

PKGD Group is a U.S.-based importer and strategic partner to a focused portfolio of producer-owned agave spirits brands from Mexico. The company was built to challenge a fundamental imbalance in the category: the people who create the product have historically captured the least long-term value from its success.

PKGD exists to change that. Over the past decade, PKGD has worked directly with multi-generational producers to bring their brands to market in the United States with disciplined execution. This includes positioning, pricing, distribution, and retail alignment designed to build real demand, not just secure placement.

The framework presented in this White Paper is drawn from that work.

PKGD operates with two non-negotiable standards:

The producer has final authority over decisions that affect the

product.

The system behind the brand holds under pressure, from

production through market execution.

These are not claims. They are requirements.

As the category enters a more disciplined phase, the market will increasingly separate brands built to endure from those built to capitalize on opportunity.

PKGD’s role is to help define that difference and execute against it.

Producer Controlled is the standard. Built Right, Brought Right, is how we win and how we hold up under pressure.

Built Right + Brought Right determines durability under pressure.

Push creates entry. Only pull sustains presence.

If push does not convert to pull over time, the model is not working.

This framework does not determine what tastes best. It determines what holds.

Initial placement is not proof of demand. Sustained velocity is.

Entry is given. Endurance is earned.

The objective is not distribution. It is conversion.

This tool is directional, not definitive.

It is designed to support decision-making under time constraints using observable signals and structural indicators.

Download the PDF

Download the PDFEn un mercado donde la visibilidad ha llegado a su punto máximo, las condiciones que determinan qué marcas lograrán perdurar han cambiado. El crecimiento ya no es suficiente para sostener a todas las marcas. A medida que la presión aumenta, la diferencia entre percepción y realidad estructural se vuelve más evidente.In a market where visibility has reached its peak, the conditions that determine which brands endure have changed. Growth is no longer sufficient to sustain every brand. As pressure increases, the difference between perception and structural reality becomes more visible.

Este documento presenta un marco para evaluar las marcas de destilados de agave más allá de las señales superficiales: Bien Construido. Bien Llevado. No es un mensaje; es un sistema para entender cómo se construyen las marcas, cómo se desempeñan en el mercado y si pueden sostenerse bajo presión. El marco combina la evaluación estructural, el comportamiento en el mercado y las señales observables para identificar qué marcas están construidas para resistir —y cuáles no.

Este marco no pretende ser una declaración de creencias. Es una herramienta para evaluar marcas bajo condiciones reales de mercado.En un mercado donde la visibilidad ha llegado a su punto más alto, las condiciones que determinan qué marcas logran perdurar han cambiado. El crecimiento ya no es suficiente para sostLos principios aquí descritos solo importan si pueden observarse, ponerse a prueba y aplicarse en la práctica.ener a todas las marcas. Conforme aumenta la presión, la diferencia entre la percepción y la realidad estructural se vuelve cada vez más evidente.

Los principios aquí descritos solo importan si pueden observarse, ponerse a prueba y aplicarse en la práctica.Este documento presenta un marco para evaluar marcas de destilados de agave más allá de las señales superficiales: Bien Construido. Bien Llevado al Mercado. Esto no es un mensaje; es un sistema para entender cómo se construyen las marcas, cómo se desempeñan en el mercado y si pueden sostener ambas cosas bajo presión. El marco combina evaluación estructural, comportamiento de mercado y señales observables para identificar qué marcas están hechas para resistir y cuáles no.

Las siguientes secciones traducen estos principios en variables observables y conductas de decisión, particularmente bajo condiciones en las que existen presiones y decisiones difíciles.

Porque en un mercado que se contrae, los resultados no dependen de la intención, sino de cómo se toman las decisiones cuando las condiciones se vuelven adversas.

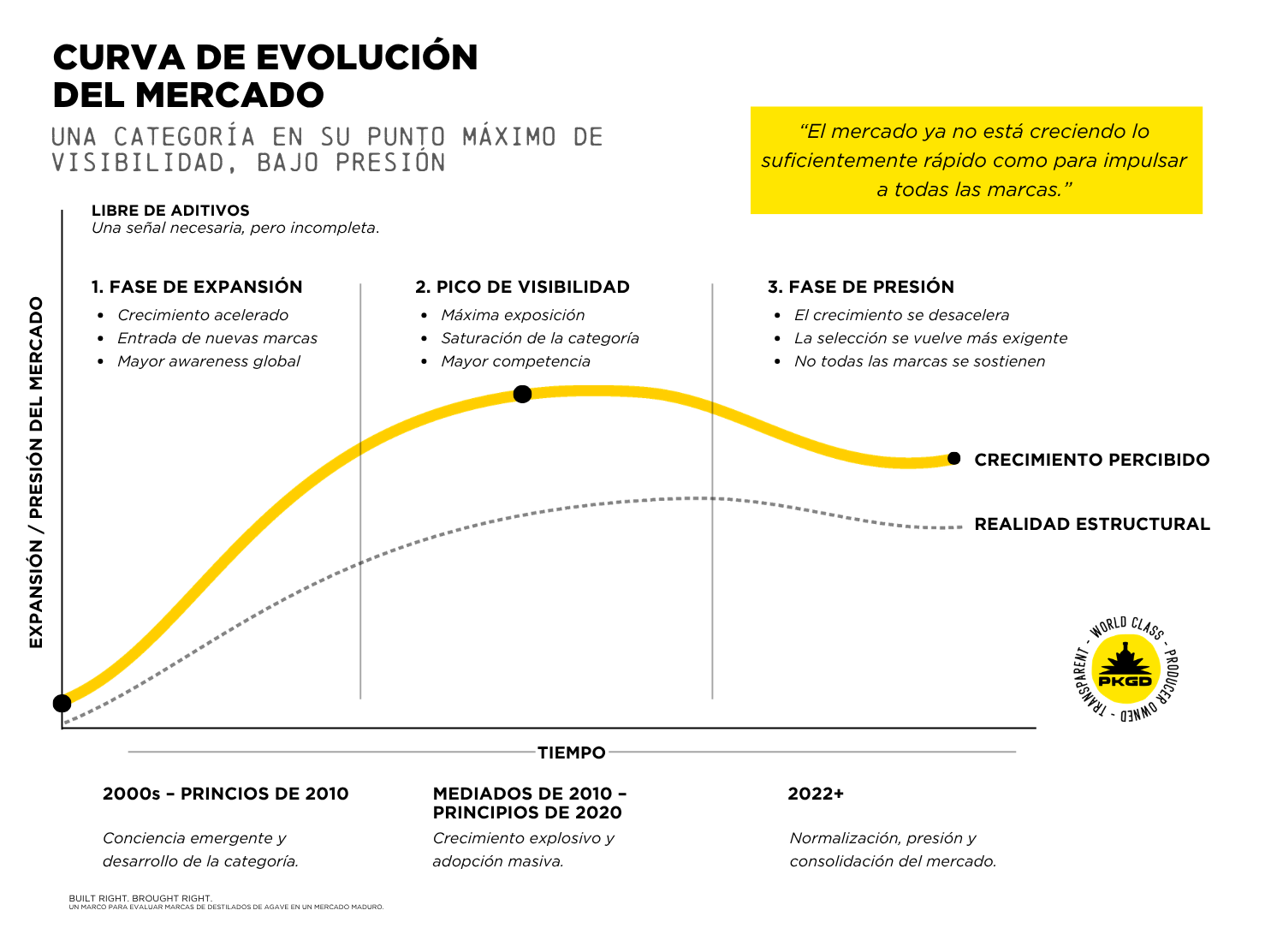

En la última década trabajando dentro de la industria del agave, hemos visto cómo la visibilidad alcanzó niveles que habrían sido difíciles de imaginar. El crecimiento fue extraordinario. Nuevas marcas ingresaron rápidamente, el interés del consumidor se expandió y el reconocimiento global alcanzó nuevas alturas.

Al mismo tiempo, la industria se volvió más difícil de navegar:

Más recientemente, el crecimiento se ha desacelerado y, en algunos casos, ha comenzado a contraerse. A medida que el impulso se estabiliza, la presión ya no es teórica: ha comenzado a sentirse. El mercado ya no se expande lo suficientemente rápido como para sostener a todas las marcas. Las marcas que ingresaron durante la expansión ahora están siendo puestas a prueba bajo restricciones reales.

Hemos visto marcas consolidarse y otras desaparecer bajo las mismas condiciones. Esto confirma que la visibilidad no determina el éxito, sino la estructura y la ejecución.

El desempeño en puntos de venta también se está volviendo más selectivo. Observamos una debilidad general en la categoría junto con un crecimiento continuo en los segmentos estructuralmente diferenciados. Las decisiones de compra están cada vez más impulsadas por la velocidad de rotación, la contribución al margen y la demanda recurrente, más que por la expansión en sí misma.

Esto ha hecho que la entrada al mercado sea más selectiva y más difícil de sostener con el tiempo.

Durante años, gran parte del debate en torno a los destilados de agave se ha enfocado en los ingredientes.

Esas conversaciones ayudaron a elevar la conciencia e impulsar la categoría.

Pero ya no son suficientes.

La transparencia en los ingredientes no responde las preguntas que realmente importan bajo presión:

En nuestra experiencia, el mercado está avanzando más allá de una conversación centrada en una sola variable.

Se requiere un marco más completo.

Estas observaciones provienen de la participación directa en construcción de marcas, distribución y ejecución en puntos de venta en múltiples mercados. No se trata de una declaración personal, sino de un marco construido a partir de patrones observados y experiencia aplicada en el mercado.

2.1 Señales del Consumidor vs Realidad Estructural

Investigaciones recientes sobre el consumidor, incluyendo el trabajo de Jay Baer, muestran un aumento en la conciencia sobre producción, transparencia y autenticidad. Estas señales representan un avance, pero siguen siendo incompletas.

Los consumidores están aprendiendo a elegir. El mercado está aprendiendo a filtrar.

El comportamiento en puntos de venta refleja un mercado en transición, donde la demanda del consumidor sigue vinculada a términos como “sin aditivos”, incluso mientras el lenguaje utilizado para clasificar esos productos comienza a cambiar. Datos recientes del mercado sugieren que el crecimiento se concentra cada vez más en los extremos: las marcas impulsadas por valor y las marcas estructuralmente diferenciadas están superando al segmento medio.

La mayoría de las señales con las que hoy se evalúan las marcas son superficiales. No permiten entender con claridad cómo responderá una marca bajo presión.

Hemos encontrado que se requiere un sistema: uno que evalúe no solo qué es un producto, sino cómo está construido y cómo llega al mercado. Este marco surge de lo que ha logrado sostenerse bajo presión, más que de la teoría por sí sola.

A medida que el mercado se vuelve más exigente, la pregunta ya no es quién puede participar, sino qué marcas pueden justificar su permanencia a largo plazo.

Dentro de este marco:

Bien Llevado determina si una marca se gana el derecho a permanecer.

El verdadero carácter de una marca se revela bajo presión. Sin embargo, no toda la presión ocurre en el punto de producción.

Algunas marcas fracasan no porque estén mal elaboradas, sino porque no llegan al mercado de una forma capaz de generar y sostener demanda. Las brechas en distribución, un posicionamiento débil y la falta de demanda por parte del consumidor pueden erosionar silenciosamente una marca, independientemente de qué tan bien esté elaborada.

Esta es la segunda dimensión de la Prueba de Presión.

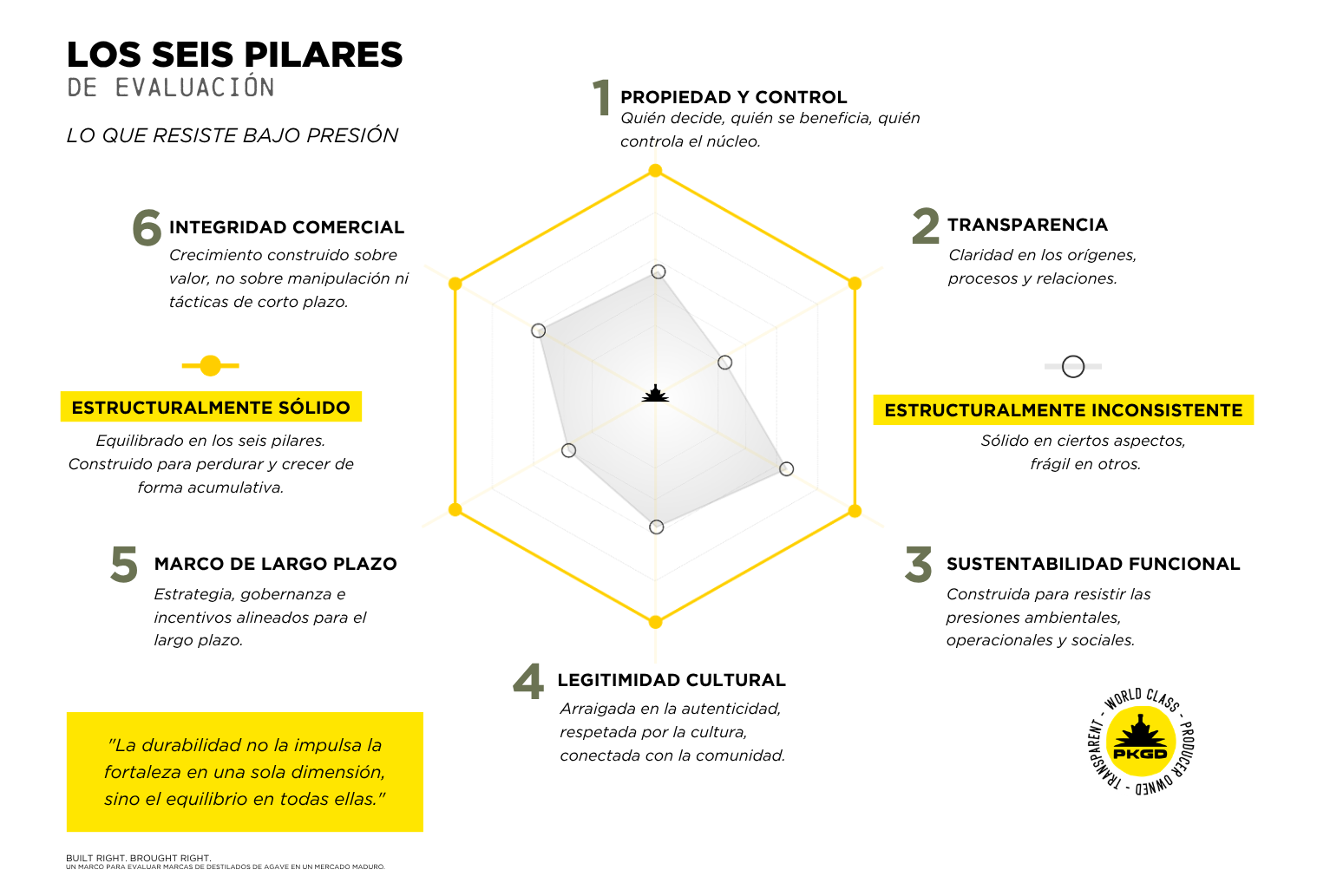

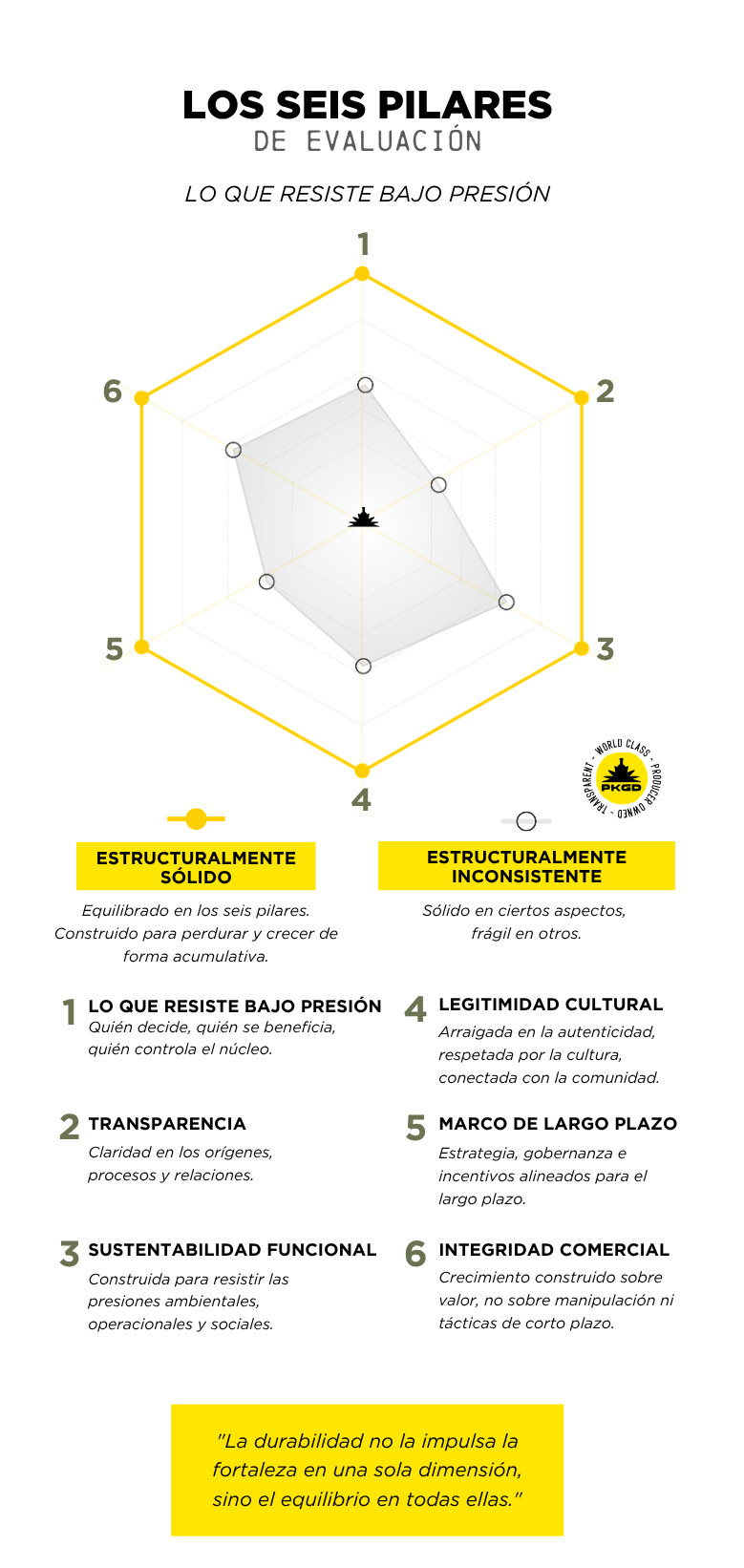

Los Seis Pilares definen las condiciones que deben mantenerse para que una marca conserve su integridad bajo presión.

Hemos observado patrones consistentes a lo largo del tiempo. Las marcas que se alinean con estos principios tienden a mantener la integridad del producto y a generar una demanda sostenible. Las que no lo hacen suelen depender de un impulso a corto plazo que resulta difícil de sostener bajo presión.

Quién es el dueño de la marca es el punto de partida; quién controla las decisiones es la prueba.

"Mantener el control sobre las decisiones de producción es lo que permite que el producto permanezca consistente, independientemente de la presión externa."

— Felipe Camarena, G4 Tequila / El Pandillo. Jesús María, Jalisco, MX.

Una marca cumple con el estándar de Bien Construida sólo si:

Sin esta base estructural, el control se vuelve condicional cuando aumentan las presiones de mercado o financieras. El Control del Productor no es una posición filosófica. Es un requisito estructural.

La participación de capital externo no descalifica a una marca; la pérdida de control sobre las decisiones, sí.

La transparencia no es una declaración; es un comportamiento.

"La transparencia es una responsabilidad, especialmente cuando se representan procesos tradicionales ante un mercado más amplio."

— Roberto Real, Tequila Ancestral Arriesgado / Tequila Selecto. Amatitán, Jalisco, MX.

La transparencia genuina incluye:

La sustentabilidad debe funcionar bajo presión.

"El agua es esencial… tratamos las vinazas y reutilizamos el agua en el proceso."

— Carlos Méndez Blas, Mezcal Palomo. Santiago Matatlán, Oaxaca, MX.

"Hemos trabajado para reducir el consumo de agua… el 100% del bagazo y las vinazas se convierten en composta."

— Eduardo Orendain Jr., Tequila Arette. Tequila, Jalisco, MX.

La sustentabilidad debe ser demostrable en la práctica, no en el discurso. Cuando la sustentabilidad no funciona bajo presión, la consecuencia no es teórica. Se vuelve operacional.

Los destilados de agave son productos culturales.

"El trabajo no es solo elaborar tequila, sino continuar un proceso que pertenece a la familia y al lugar."

— Chava Rosales, Cascahuín. El Arenal, Jalisco, MX.

La legitimidad refleja:

Cuando esta conexión se rompe, la legitimidad no desaparece de inmediato. Se erosiona con el tiempo.

El crecimiento a corto plazo no es el objetivo. La durabilidad sí.

"Las decisiones se toman pensando en las generaciones futuras."

— Juan Eduardo Núñez, Tequila El Viejito. Atotonilco, Jalisco, MX.

"Preferimos crecer de forma sostenible, sin atajos."

— Eduardo Orendain Jr., Tequila Arette. Tequila, Jalisco, MX.

"El crecimiento tiene que respetar el ritmo de la tierra."

— Fausto Romero, Raicilla El Acabo. El Asil. Ahuacatepec, Jalisco, MX.

El impulso puede acelerar el crecimiento. También puede ocultar debilidades estructurales.

La integridad comercial no solo consiste en proteger una marca. Consiste en construir una demanda real y sostenida.

"La responsabilidad se extiende más allá de elaborar el producto… a cómo se representa en el mercado."

— Luis Ángel Villalobos, Tequila El Ateo. Romita, Guanajuato, MX.

"Todos queremos crecer… pero debe hacerse con ética y contribuyendo a la comunidad."

— Sergio Vivanco, Destilería Viva México. Arandas, Jalisco, MX.

Bien Llevado requiere:

Determina si un producto puede perdurar.

Bien Construido no es un concepto abstracto. Está definido por variables estructurales evaluables, que incluyen:

La presencia de estas variables no es suficiente por sí sola. La pregunta crítica es si resisten bajo presión.

Determina si un producto sobrevive comercialmente.

Bien Llevado se expresa a través del comportamiento observable en el mercado. Las variables clave incluyen:

En un mercado que se contrae, los principios no existen de forma aislada. Se ponen a prueba a través de compromisos difíciles. Los puntos de presión más comunes incluyen:

Estos momentos no son excepciones. Son las condiciones que definen los resultados.

La diferencia entre las marcas que perduran y las que no no está en enfrentar presión, sino en cómo toman decisiones bajo ella.

Las marcas que mantienen la integridad en la toma de decisiones bajo presión protegen el valor de largo plazo del producto.

Las que no lo hacen pueden lograr ganancias a corto plazo, pero introducen una erosión estructural con el tiempo.

La reestructuración del panorama de distribución en EE. UU. refuerza un argumento central de este documento: el acceso al mercado no es lo mismo que la ejecución en el mercado.

A medida que los modelos de distribución nacional enfrentan presión, los proveedores ya no priorizan la cobertura teórica en los 50 estados. Priorizan la confiabilidad operacional, la solidez regional y la capacidad de generar resultados a nivel de cuenta.

Los movimientos recientes entre los principales distribuidores reflejan este cambio. Las grandes plataformas nacionales se están fragmentando en operadores regionales con una ejecución local más sólida, mientras otras están expandiendo capacidades en cerveza, destilados y nuevas categorías de bebidas para mantenerse relevantes.

Esta no es solo una historia de distribución. Es una señal estructural.

El nivel intermedio de la cadena atraviesa la misma prueba de presión que las marcas.

Bajo presión, la pregunta ya no es quién puede cargar la mayor cantidad de marcas. La pregunta es quién puede generar enfoque, impulsar rotación y convertir presencia en demanda recurrente.

Para las marcas controladas por el productor, esta distinción es crítica. Estar en el catálogo no es suficiente. Contar con apoyo activo en los mercados correctos, con incentivos alineados y ejecución clara, es lo que determina si la integridad de producción se traduce en crecimiento sostenible.

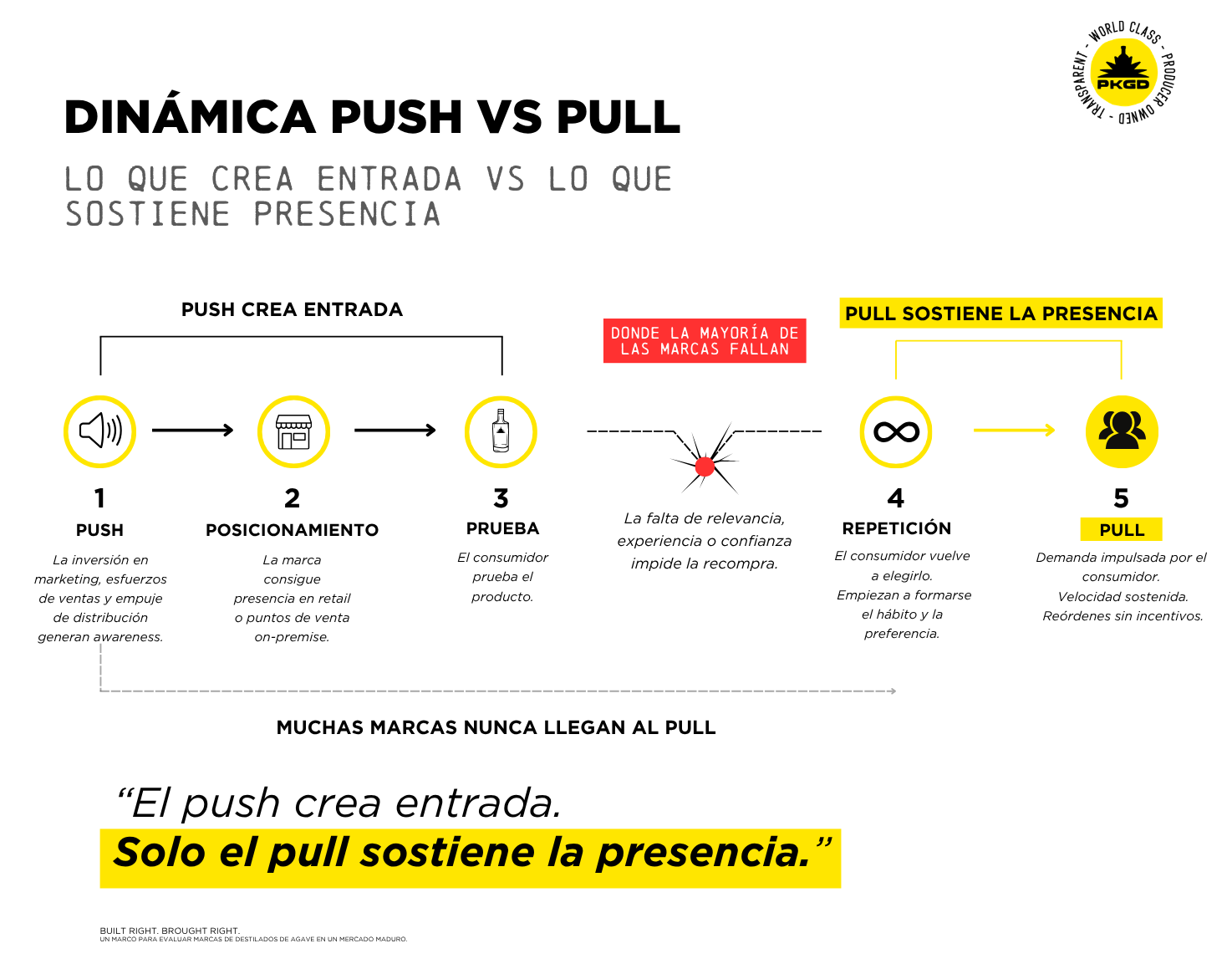

El impulso comercial es necesario para entrar al mercado, pero si ese impulso no logra convertirse en demanda real, la marca termina dependiendo permanentemente de él.

Bien Llevado también implica que un producto pueda ser descubierto, entendido y correctamente presentado en el punto de búsqueda y venta. Esto incluye cómo se clasifica, cómo se describe y qué tan fácil es para el consumidor comprender qué lo diferencia dentro de un mercado saturado.

Algunas señales observables de demanda real (“pull”) incluyen:

Todas las marcas requieren apoyo.

La diferencia está en si ese apoyo fortalece una demanda existente o sustituye la ausencia de ella.

Cuando el impulso comercial sostenido no logra convertirse en demanda real, el riesgo a largo plazo aumenta tanto para la marca como para el punto de venta.

En la práctica, este riesgo suele reflejarse en patrones consistentes:

Si una marca no demuestra una transición de impulso comercial a demanda real con el tiempo, debe ser reevaluada, independientemente de su éxito inicial en distribución.

Este marco no evalúa productos por sabor.

Evalúa si la estructura protege al producto de ser modificado por presión comercial.

Algunas marcas están correctamente elaboradas en todos los niveles de producción, pero fracasan por una ejecución débil. Esto no es un fracaso del producto; es un fracaso de mercado, y el resultado es el mismo.

Hemos participado en estas decisiones en tiempo real y observado una división fundamental del trabajo:

Cuando ambos están alineados, el sistema funciona.

Este marco no es un sistema de cumplimiento. Sin embargo, la demanda real y la ejecución efectiva se pueden observar a través de señales como:

Estas señales ayudan a distinguir la demanda estructural del desempeño temporal. No definen el éxito; indican si ese éxito es real.

Otros indicadores pueden incluir una conversión efectiva en búsquedas, expansión después de un buen desempeño en mercados piloto y compras recurrentes posteriores a degustaciones guiadas o experiencias asistidas.

Lo que importa no es lo que dice una marca.

Lo que importa es cómo está construida y cómo se desempeña bajo presión.

BUILT RIGHT. BROUGHT RIGHT. No es un mensaje. Es un sistema de evaluación.

Este marco no es un sistema de certificación. Es una herramienta para evaluar la estructura y el desempeño bajo presión. Específicamente:

A través de regiones y tradiciones, el mensaje se mantiene consistente. Los siguientes productores y socios representan la integridad estructural y el comportamiento de mercado definidos por este marco.

Tequila (Jalisco y Guanajuato)

Mezcal

Raicilla

Diferentes regiones. Diferentes tradiciones. Principios alineados: responsabilidad, disciplina y continuidad.

A medida que aumenta la presión, la diferenciación se vuelve más clara. El mercado no recompensará a todas las marcas. Recompensará a las que resistan.

Pero este momento no es solo un filtro.

Es un cambio.

Durante años, el crecimiento permitió que muchas marcas participaran sin ser plenamente probadas. La visibilidad creó la apariencia de fortaleza. El listing creó la apariencia de demanda. El impulso enmascaró las debilidades estructurales.

Esa etapa está terminando.

A medida que el mercado se contrae:

Lo que comienza a importar ahora es si una marca puede convertir su estructura en demanda sostenida. No una vez, sino de manera repetida. Bajo presión.

Aquí es donde la diferencia entre Bien Construido y Bien Llevado se vuelve decisiva.

Ambas fracasan. Solo que a ritmos distintos.

La presión no surge únicamente del declive.

Con frecuencia, también es consecuencia del éxito.

El crecimiento introduce sus propias tensiones:

Lo que logra sostenerse bajo estas condiciones es lo que define los resultados a largo plazo.

La oportunidad no es simplemente sobrevivir a este cambio.

Es salir de él con claridad.

Para entender no sólo qué es una marca, sino cómo se comporta cuando es puesta a prueba.

Para construir sistemas que no dependan de condiciones ideales.

Para alinear producción, posicionamiento y ejecución de mercado de una manera que pueda sostenerse con el tiempo.

En un mercado menos indulgente, la claridad se convierte en ventaja. Y para quienes están bien construidos y bien llevados, la presión no es una amenaza. Es validación.

Para los distribuidores, este marco ofrece una forma de evaluar qué marcas convertirán la demanda en velocidad de rotación sostenida, y no solo en listing inicial.

Para los retailers, ofrece una forma de distinguir entre marcas que generan compra repetida y las que dependen de apoyo continuo para mantener el movimiento.

Para los dueños de marcas, define las condiciones necesarias para construir un negocio que pueda perdurar más allá del crecimiento inicial y operar de manera consistente bajo presión.

En la práctica, la aplicación no es teórica. Se manifiesta en decisiones:

El objetivo no es optimizar para el ingreso.

Es construir para la permanencia.

En cada caso, la pregunta es la misma:

¿Está esta marca estructuralmente posicionada para sostener su desempeño a medida que las condiciones se endurecen, o depende de condiciones que podrían no mantenerse?

Estar bien construida no es suficiente. Una marca también debe distribuirse al mercado de una manera que crea y sostenga una demanda real.

En última instancia, el mercado determina qué marcas resisten y cuáles no.

Este marco es un intento de comprender por qué.

No es una teoría construida en aislamiento. Refleja patrones observados entre productores, marcas, distribuidores y retailers que operan bajo condiciones reales.

A través de esas observaciones, una verdad se vuelve consistente:

Sin demanda, la disciplina se vuelve irrelevante.

Sin disciplina, la demanda se vuelve destructiva.

Las marcas que perduran no se definen por una sola ventaja. Se definen por la alineación:

Esto es lo que permite a una marca navegar la presión sin comprometer lo que la hizo valiosa en primer lugar.

Este marco no determina qué sabe mejor.

Determina qué resiste.

La siguiente etapa de la industria no estará definida por quién participa.

Estará definida por quién está estructurado para resistir presión y quién no.

El crecimiento continuará, pero no de manera uniforme.

La atención seguirá presente, pero no indefinidamente.

Y la distancia entre percepción y realidad seguirá reduciéndose.

El mercado ya no pregunta quién puede entrar.

Está revelando quién puede permanecer.

BUILT RIGHT. BROUGHT RIGHT. No es un mensaje, es un estándar.

Todos los testimonios de productores incluidos en este documento fueron recopilados directamente a través de entrevistas, respuestas escritas y conversaciones documentadas entre enero y marzo de 2026.

Las citas han sido traducidas y editadas para mayor claridad cuando fue necesario.

Su inclusión aporta perspectiva desde dentro de la categoría y no implica el respaldo a este marco ni a sus conclusiones.

PKGD Built Right. Brought Right.

Propósito: Ser una herramienta de evaluación rápida para determinar si una marca está estructuralmente sólida y es comercialmente viable bajo presión.

1. Control

¿El productor conserva la autoridad final e irrevocable sobre las decisiones que afectan al producto?

☐ Sí ☐ No

2. Consistencia Bajo Presión

Si los costos aumentan o la oferta de agave se restringe, ¿es probable que el producto permanezca sin cambios?

☐ Sí ☐ No

3. Transparencia como Comportamiento

¿Se demuestra la transparencia a través de acciones, no solo de declaraciones?

☐ Sí ☐ No

4. Sustentabilidad que Funciona

¿Las prácticas ambientales y de producción son operativas y se mantienen bajo presión?

☐ Sí ☐ No

5. Legitimidad Cultural

¿El producto está significativamente conectado con su territorio, proceso y comunidad?

☐ Sí ☐ No

Resultado Bien Construido:

☐ Sólido (4–5 Sí)

☐ Condicional (2–3 Sí)

☐ Débil (0–1 Sí)

6. Generación de Demanda

¿Hay evidencia clara de demanda del consumidor más allá del listing inicial?

☐ Sí ☐ No

7. Conversión (Push a Pull)

¿El apoyo inicial se convierte en compras repetidas y reórdenes?

☐ Sí ☐ No

8. Consistencia de Rotación

¿El producto tiene una rotación consistente en cuentas comparables?

☐ Sí ☐ No

9. Integridad de Precios

¿La marca mantiene su precio sin depender de incentivos continuos?

☐ Sí ☐ No

10. Claridad en Anaquel y Búsqueda

¿El producto es fácil de entender, categorizar y diferenciar en el punto de venta?

☐ Sí ☐ No

Resultado Bien Llevado:

☐ Sólido (4–5 Sí)

☐ Condicional (2–3 Sí)

☐ Débil (0–1 Sí)

PKGD Group es un importador estadounidense y socio estratégico de un portafolio selecto de marcas de destilados de agave controladas por el productor, provenientes de México. La empresa fue construida para desafiar un desequilibrio fundamental en la categoría: las personas que crean el producto han capturado históricamente el menor valor a largo plazo de su éxito.

PKGD existe para cambiar eso. Durante la última década, PKGD ha trabajado directamente con productores multigeneracionales para llevar sus marcas al mercado de los Estados Unidos con una ejecución disciplinada. Esto incluye posicionamiento, precios, distribución y alineación en punto de venta diseñados para construir demanda real, no solo asegurar listings.El marco presentado en este documento surge de ese trabajo.

Refleja una realidad simple: el producto por sí solo no determina el éxito, y el impulso sin estructura no dura.

PKGD opera con dos estándares no negociables:

Estos no son declaraciones. Son requisitos.

A medida que la industria entra en una etapa más disciplinada, el mercado comenzará a distinguir cada vez más entre las marcas construidas para perdurar y aquellas construidas para capitalizar una oportunidad.

El rol de PKGD es ayudar a definir esa diferencia y ejecutar contra ella. El control del productor es el estándar.“BUILT RIGHT. BROUGHT RIGHT.” Define cómo construimos crecimiento sostenible y cómo nos mantenemos sólidos bajo presión.

Bien Construido + Bien Llevado determina la durabilidad bajo presión.

El impulso comercial permite entrar al mercado. Solo la demanda real permite permanecer.

Si ese impulso no se convierte en demanda sostenida con el tiempo, la estructura no está funcionando.

La distribución inicial no valida una marca. La rotación consistente y la recompra sí.

El objetivo no es únicamente lograr presencia, sino construir demanda recurrente.

La entrada puede impulsarse. La permanencia debe ganarse.

Este marco no evalúa qué producto sabe mejor. Evalúa qué estructuras pueden sostener integridad bajo presión.

Este marco es una herramienta de orientación, no una conclusión definitiva.

Su propósito es apoyar la toma de decisiones mediante señales observables e indicadores estructurales, especialmente en contextos donde el tiempo y la información son limitados.

Descarga el PDF

By accessing and using PKGD´s website, you agree to the cookie policy outlined in our privacy notice.

By accessing and using PKGD´s website, you agree to the cookie policy outlined in our privacy notice.